What Is a Bi-Weekly Mortgage Calculator?

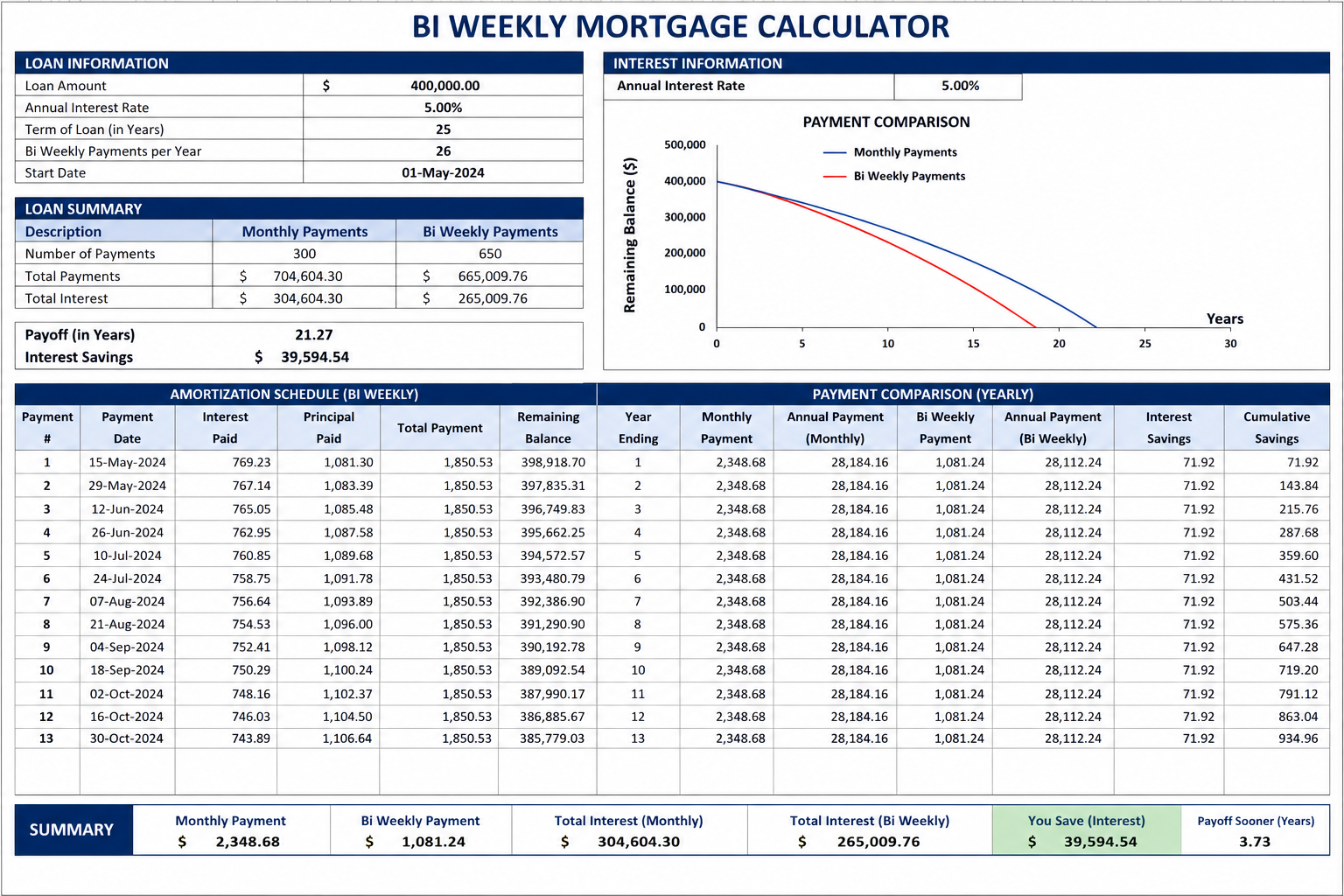

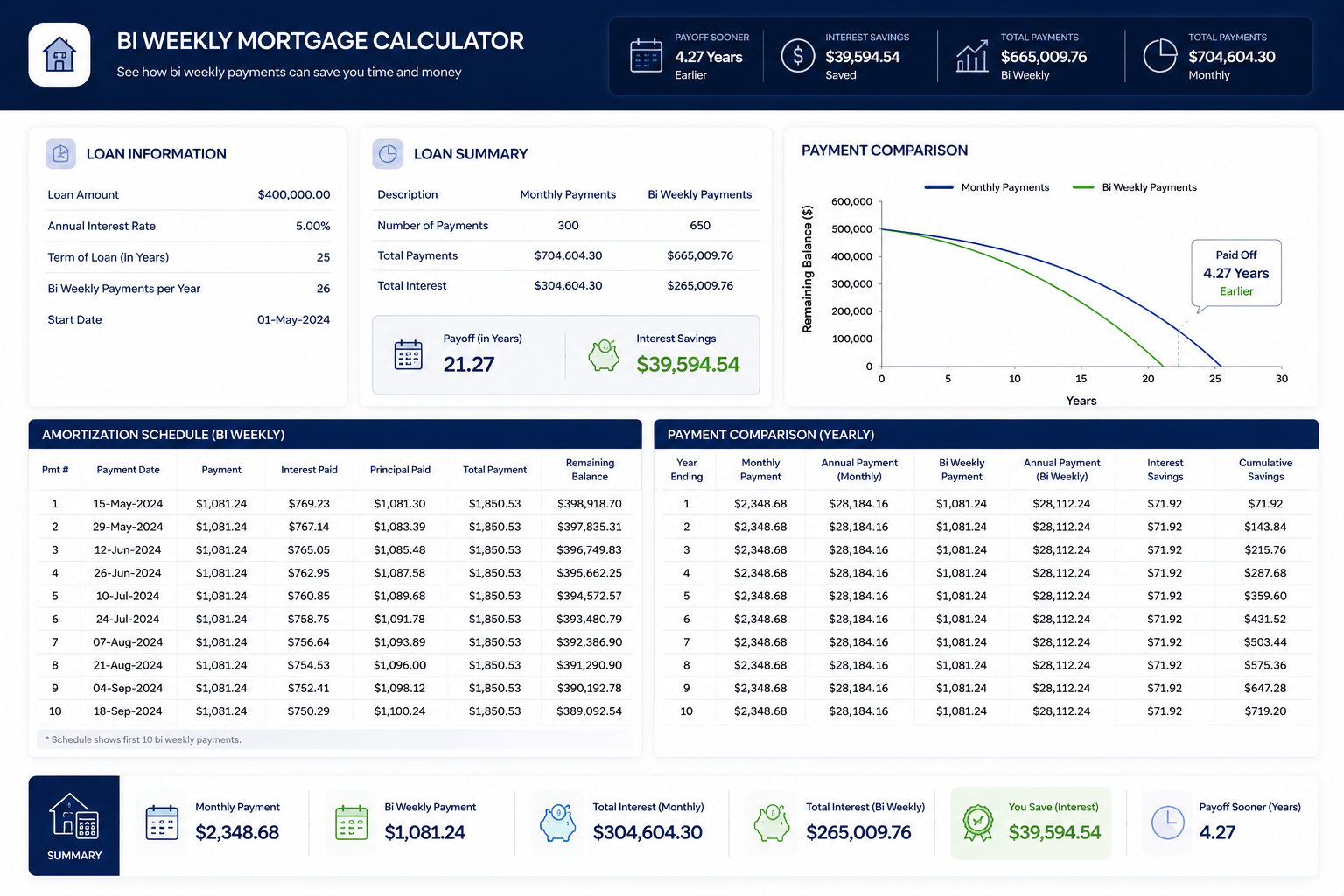

A bi-weekly mortgage calculator shows what happens to your loan when you pay half your monthly mortgage payment every two weeks instead of a single payment once a month. Because a year has 52 weeks, paying every two weeks adds up to 26 half-payments — the equivalent of 13 full monthly payments instead of the usual 12. That one extra payment a year goes straight toward your principal, which is why a bi-weekly schedule consistently saves homeowners both interest and years on the loan.

Use this free bi-weekly mortgage calculator to enter your loan amount, interest rate, and term, then instantly see your bi-weekly payment amount, total interest saved, and exactly how much sooner your mortgage will be paid off compared to a standard monthly schedule.

Monthly vs. Biweekly Mortgage Calculator: What's the Real Difference?

The most common question homeowners ask is how a monthly vs. biweekly mortgage calculator actually differs in the numbers. On paper, a bi-weekly payment looks like simply "half the monthly payment," but the impact compounds significantly over time because of how amortization works.

| Factor | Monthly payments | Bi-weekly payments |

|---|---|---|

| Payments per year | 12 | 26 (equal to 13 monthly payments) |

| Extra principal paid per year | $0 | One full extra monthly payment |

| Typical interest saved on a 30-year loan | — | Tens of thousands of dollars |

| Typical time saved | — | Roughly 4–6 years |

This calculator runs both scenarios side by side, so instead of guessing, you can see your specific monthly payment, your specific bi-weekly payment, and the exact dollar amount and time difference between the two.

Biweekly Mortgage Calculator With Extra Payments

If you want to pay your mortgage off even faster, the calculator above also supports extra payments. Enter any additional amount in the "Extra per bi-weekly payment" field and it will be applied directly to your principal balance on top of the standard bi-weekly amount. Even a modest extra payment — $25 or $50 every two weeks — can meaningfully shorten your loan term and reduce total interest, since every extra dollar is removed from the balance before it has a chance to accrue interest.

Bi-Weekly Mortgage Calculator With Taxes and Insurance (Escrow)

Your bi-weekly payment plan only affects principal and interest (P&I) — the part of your mortgage you control directly. Property taxes and homeowners insurance are usually collected separately by your lender into an escrow account and paid out on your behalf, so switching to bi-weekly payments does not reduce those costs. To give you a realistic full picture, you can optionally enter your annual property tax and insurance amounts here. The tool then estimates your total monthly housing cost (P&I equivalent plus the prorated escrow amount), so you can budget accurately rather than looking at principal and interest in isolation.

Bi-Weekly Payments on a 30-Year Mortgage

The 30-year fixed mortgage is the most common loan in the US, which is also where bi-weekly payments make the biggest difference. Because interest accrues over such a long period, the extra annual payment from a bi-weekly schedule has decades to compound in your favor. In a typical scenario — for example a $300,000 loan at 6.5% — switching from monthly to bi-weekly payments can cut the loan term by several years and save a substantial amount in total interest, without changing your interest rate or refinancing. Enter your own loan amount, rate, and term above to see the exact figures for your situation rather than a generic example.

Free Bi-Weekly Mortgage Calculator vs. Building One in Excel

Some homeowners search for a bi-weekly mortgage calculator Excel template so they can build their own amortization schedule using formulas like PMT and a manual 26-period loop. That approach works, but it takes time to set up correctly and it's easy to make small errors in the period count or rate conversion that throw off the results. This page gives you the same output instantly: enter your numbers once and get your bi-weekly payment, total interest saved, and new payoff date immediately, with no spreadsheet required and nothing to download.

How the Bi-Weekly Mortgage Calculation Works

The calculator first computes your standard monthly mortgage payment using your loan amount, interest rate, and term. It then simulates a bi-weekly schedule where half of that monthly payment (plus any extra amount you specify) is paid every two weeks, with interest accruing on the remaining balance each period. The results compare total interest paid and total payoff time under both schedules, so the savings you see reflect real amortization math rather than a rough estimate.

Frequently Asked Questions

How much can a biweekly mortgage payment save you?

On a typical 30-year mortgage, switching to bi-weekly payments can save tens of thousands of dollars in interest and cut roughly 4 to 6 years off the loan term, depending on your loan amount and interest rate. Adding even a small extra payment increases the savings further.

Will my lender automatically apply bi-weekly payments correctly?

Not always. Some lenders simply hold your bi-weekly payments and apply them once a month, which removes the benefit of extra principal reduction. Confirm with your loan servicer that bi-weekly payments are applied immediately to principal, or make a manual extra principal payment once a year for the same effect.

Does this calculator include taxes, insurance, or PMI?

The core calculation focuses on principal and interest, which is what a bi-weekly schedule actually changes. You can optionally add annual property tax and insurance figures to estimate your total monthly housing cost, including a typical escrow contribution.

Is a bi-weekly mortgage calculator with extra payments worth using?

Yes — it gives a far more accurate payoff projection than a basic calculator, since most homeowners who switch to bi-weekly payments also add at least a small extra amount when they can.

Why Use Mortgage Calculator Pro's Bi-Weekly Mortgage Calculator

This calculator is completely free, requires no account or email, and runs the full bi-weekly amortization calculation directly in your browser. Every formula is based on standard amortization mathematics used across the mortgage industry, so the numbers you see here — bi-weekly payment, interest saved, and new payoff time — are ones you can trust when deciding whether a bi-weekly mortgage plan makes sense for you.